.png?width=2708&height=560&name=2022%20Render%20Capital%20Red-04%20(4).png "2022 Render Capital Red Logo")

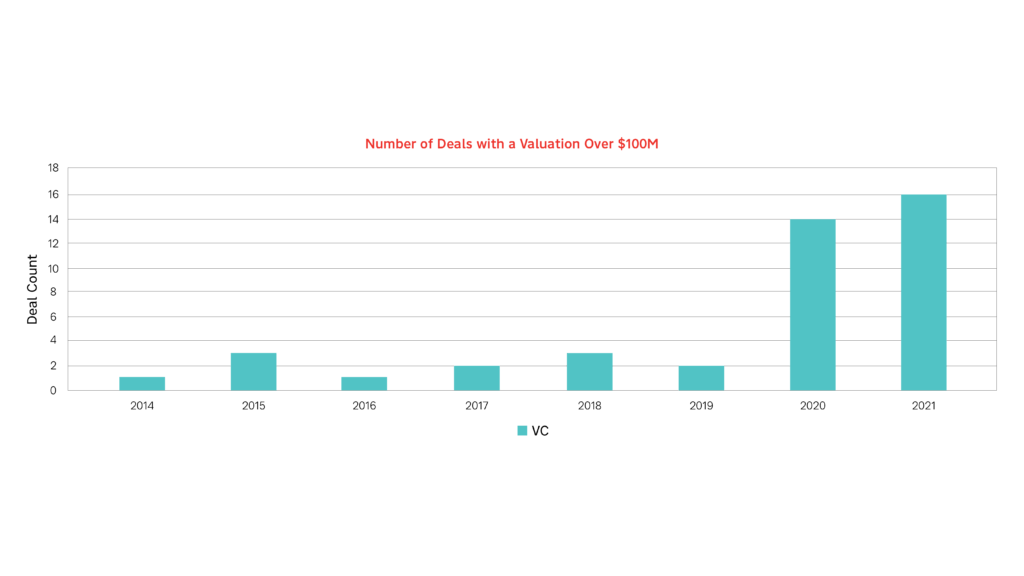

The valuation process of a startup is similar to the price determination process of a product as it goes through the distribution channel. The sellers (and resellers) set the price of a product based on their desired profit margins. For a price-sensitive product (e.g. coffee beans), the higher the price / cost in the early phases of the distribution channel, the lower the profit margins. While for a demand price inelastic product (e.g. concert tickets), an increase in the price may not affect the seller’s (resellers) profit margin because they can pass on that cost to the end consumer/ final buyer. Valuations are important to startup founders and investors because it reflects the perceived earnings potential of the business through the lifetime of the company. In 2020, the number of seed-stage deals with a post-money valuation of $100 million were more than the previous five years combined. From 2014 to 2019, there were 12 seed-stage deals in the U.S. with a post-money valuation above $100 million. While in 2020, there were 14 seed-stage deals in the U.S. with a post-money valuation above $100 million. That trend seems to continue into 2021, as the number of seed stages in the U.S. with a post-money valuation above $100 million has already surpassed that of 2020 (16 > 14).

The median and average post-money valuations of US-based seed-stage deals have consistently been on the rise since 2013. The average seed-stage post-money valuation rose from $6.5 million in 2013 to $14.2 million in 2020. While the median seed-stage post-money valuation rose from $5.6 million in 2013 to $10.0 million in 2020. This growth in valuations has been attributed to the abundance of capital in the seed stage market. Especially as major later-stage investment firms enter the market. In 2021, Sequoia, Index Ventures, Andressen Horowitz and Greylock Partners all announced seed-stage focused funds with a combined value of $1.3 billion.

To put that in perspective, in the first three quarters of 2021, the seed-stage market invested $8.6 billion into firms according to the Q3 Pitchbook – NVCA Venture Monitor. These freshly minted funds make up a whopping 15% of the total invested capital into seed-stage companies in the first three quarters of 2021. As later stage rounds get more competitive, multistage firms aim to secure less expensive stakes in promising startups at earlier stages. Thus, seed-stage deals with $100 million post-money valuations may become more common in the years to come. In his recent article, Fred Wilson, Partner at Union Square Ventures, warns against the trend of valuations this high at the seed stage. He states some reasons why this trend concerns him as an investor. Two of which were 1) the high failure rate of seed-stage startups and 2) the dilution that occurs from seed to exit. From personal experience, Fred Wilson has seen that from seed to exit, a seed-stage investor’s ownership stake will get diluted by around 66.67%. And, according to a report by Radicle, 97% of startups fail between seed to exit.

Wilson goes on to explain a model that backs up his point. Below are the assumptions behind the model:

- Fund Size: $100,000,000

- Number of Investments: 100

- Post-Money Value: $100,000,000

- Investment Amount: $1,000,000

- Ownership: 1.00%

- Average Dilution from Seed to Exit: 66.67%

- Top-Performing Investment Outcome: $10,000,000,000

- Power Law Number: 0.75

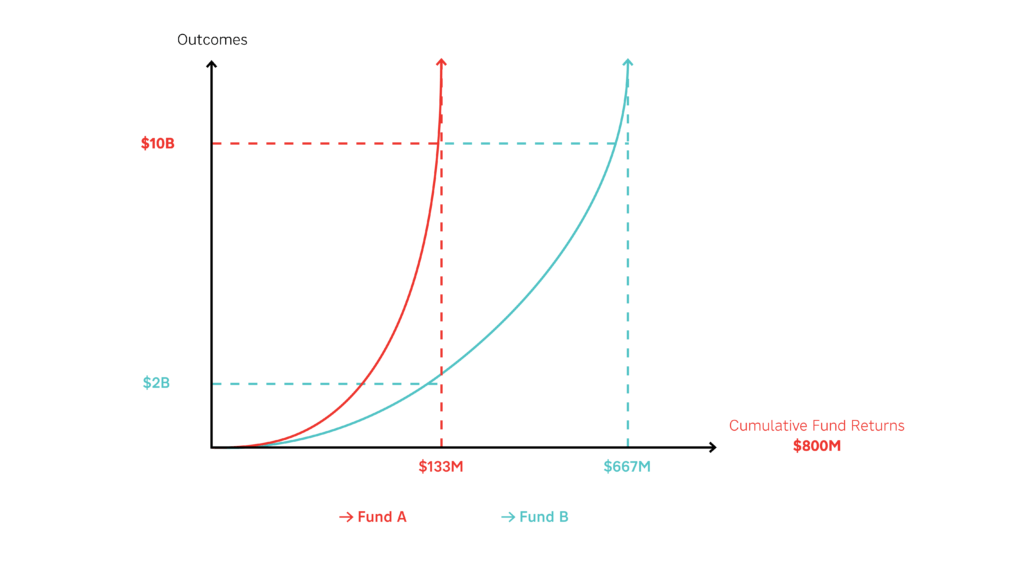

The outcome of the modeled fund was a total value at exit of $133,333,323 and a multiple fund return of 1.33x. The point Fred is trying to make is that the probability of achieving positive fund returns if they invest solely in $100mm seed stage deals is low. Since 2012, there have only been 14 VC – backed companies that have had exits over $10 billion. The possibility of a startup exiting at $10 billion is very low, that being said Fred chose an optimistic best possible outcome in his fund model and was still only able to achieve a modest overall fund return of investment (1.33x) Venture capital, especially at the seed stage is a game of probability. Investors value companies based on their probability to achieve the desired outcomes that will lead to positive fund returns.

That is why Fred advocated for seed rounds with a post-money valuation in the lower eight-digit range. We reimagined the model he built for a fund that invested the same check size into seed rounds with a post-money valuation of $20mm. The ownership stake as of that round would be 5% as opposed to 1% in a $100mm post-money seed round. We kept all other assumptions the same. The outcome for our model achieved a fund return of 6.67x and has a total value at an exit of $666,666,617.

Let’s name the $100 mm post-money fund, Fund A and the $20 mm post-money fund, Fund B. Keeping the top-performing outcome the same, Fund B would outperform Fund A five times over. Fund B would only need a top-performing investment outcome of $2 billion to achieve similar returns that Fund A produced with a top-performing investment outcome of $10 billion. Since 2012, over 130 VC-backed companies have exited at valuations of at least $2 billion. Hence there is a higher likelihood of Fund B achieving positive fund returns than Fund A. View the calculations here.

To restate, the message Fred was trying to convey to readers in his article was that lower seed-stage valuations lead to better outcomes for investors at that stage. He makes a convincing point by modeling out a potential fund scenario with given parameters. We believe that there is an even deeper insight that can be gained from the article. That insight is the inductive reasoning process investors make while considering a potential investment. This is the process with which investors think about the potential value of an investment into a startup in relation to the overall desired performance of the fund. Founders can leverage this framework to better prepare for an investor’s diligence & negotiation process.

For instance, if a founder is asked, “what is the size and the growth stage of the target market?” The founder can prepare for this question by thinking about how the potential share of the market they hope to acquire could translate into returns for the fund. A good answer may be, “The size of our market is ‘X’ and is expected to grow at a rate of ‘Y’% each year over the next 10 years. At which point we hope to have acquired ‘Z’% of the market. Using the average enterprise value-to-revenue valuation multiple (EV/R) of recent exits in our industry, our company could be worth $‘K’ billion. Another good question an investor might ask is “what is the exit activity in the industry over the past ‘x’ years?” Founders can best answer this question by knowing that investors are truly asking “what is the likelihood of a liquidation event?”. Investors see this as an opportunity to earn returns to the fund. Founders can also utilize this framework in the negotiation process with lead investors. Economic terms, such as participation rights, liquidation preference and pro-rata rights to name a few, are put in place based on the perceived risk to investors.

To conclude, Fred Wilson’s message is that lower valuation seed-stage rounds are more likely to lead to positive fund returns for investors. It is important for founders to keep this in mind and recognize that investors base decisions on the probability of an investment to achieve the desired returns for the fund. Founders should take the approach of thinking about how a potential investment into their company could lead to the desired returns for the investors fund when undergoing the diligence process. The more information founders know about a fund and its recent performance, the better prepared they will be for the investors diligence & negotiation process. This principle is valuable for founders in the fundraising process regardless of the valuations of the firm.

Render Capital is a $15 million fund focused on investing into early-stage companies in the Louisville and Southern Indiana area. The goal of the fund is to increase access to capital within the region, thus we invest through equity, debt and other alternatives to equity financing instruments into early-stage companies. Now that you know more about us, feel free to reach out to us. We would be happy to learn more about what you are building in our region.